By Stefan M. Kløvning

Washington D.C., Economics – A dark cloud has been hanging over the American people for the past decades, one going increasingly bigger and darker, and one may wonder when it may, at last, begin to rain, or whether it has already started. This cloud is the American federal debt, which is currently running at $21 trillion and growing. Many an American reader has at one point asked himself the questions: How will this influence myself and my future? And how about my children, and grandchildren? How long can the problem be put off, any more than the bubble causing the financial crisis of 2008?

To fix a problem, one must comprehend how it appeared in the first place. From the data available, one may go all the way back to George Washington in 1791 (no data from 1789-90), where the debt stood at roughly $75 million, which indicates that the U.S. has always been in some federal debt. There are many important details from the 1800s which will be mentioned here, especially under Abraham Lincoln, but the main emphasis will be placed on the era of Franklin D. Roosevelt and forward, as that’s when the debt really began to grow exponentially worse.

When Theodore Roosevelt first assumed office in 1901, the federal debt was about $2 billion, which was far below what it was under Andrew Johnson between 1865-1869, with a high point of $2.773 billion in 1866. Between Johnson and Roosevelt, there was even a low point of $1.5 billion after a rigorous effort to decrease the federal debt. The trend didn’t turn for long, and the debt kept growing almost continuously under Grove Cleveland and William McKinley, with exceptions in 1893 of $42.5 million reductions, the year Cleveland assumed office and McKinley’s reductions of $21 million in 1898. In essence, the federal debt fluctuated in the 1800s with comparatively low numbers compared to how big the debt is today, but an important statistics to include pre-1900s is the debt increase of 2,700% under four years of Abraham Lincoln, from $90 million to $2.7 billion in the midst of the civil war, the biggest % increase in the national debt ever. And though, as said, there was a rigorous attempt to reduce it between Johnson and Teddy Roosevelt, it turned out to be an irreversible measure.

Before going over the real increase from $2 billion to $20 trillion in the next two centuries, the significance of ‘Abe’s debt revolution’, if it may be so called, must be further stressed. The great orator may be greatly admired for his upsides, like his achievement of the emancipation proclamation, but in an analysis of the federal debt, it must not lead us to cover our eyes from his role in the greatest percentile increase in the federal debt ever seen in the United States. In addition to economic difficulties arising from a civil war in itself, it didn’t help much that merchants and financiers linked to the South were in fierce opposition to Lincolns presidency. Despite all this, Lincoln refused financial help from the English bank and the Rothschilds during the Civil War even though the government was broke even before it began, so how did he finance it? One solution was to borrow money from the public. Treasury official Lucius Chitterson recalled a statement by Treasury Secretary Salmon P. Chase during a conference early in the war,

There is money enough in the loyal North and West to pay for suppressing this wicked rebellion. The people are willing to loan it to their Government. If we cannot find the way to their hearts, we should resign and give place to those who can. I am going to the people! If there is a farmer at the country cross-roads who has ten dollars which he is willing to loan to the Government, he shall be furnished with a Treasury obligation for it, without commission or other expense. When we have opened the way directly to the people and they fail to respond to the calls of their Government in the stress of civil war, we may begin to despair of the republic!

Lincoln had left the administration of the Treasury Department completely in Chase’s hands as he proclaimed himself to be ‘ignorant of financial and economic matters.’ He did, however, still manage to borrow money from the banks to help finance the war. According to economic historians William Schultz and M. R. Caine, ‘no bankers had no great love for the Republicans, but they responded loyally to the Administration’s call for financial cooperation,’ when Lincoln sought to finance the war without congressional approval. As such, the debt grew and grew, and in 1864, Lincoln at last conceded, “[The Civil War] has produced a national debt and taxation unprecedented, at least in this country.” One may yet reflect upon this whether this unprecedented growth was inevitable due to the circumstances of the Civil War or whether Lincoln, Chase, and the rest of the Treasury could do anything which would reduce that growth, and whether that reduction would impede their chances of success in the war.

After three decades efforts had been made to reduce the federal debt, the trend turned by 1894, and Theodore Roosevelt had to pick it up at the beginning of the 20th century at almost the same level as Lincoln left it. In his eight years as President, however, he didn’t increase the debt more than 22.9%, which is miniature compared to Woodrow Wilson’s 804.8%, from 1913 to 1920 in the midst of the First World War. According to Andrew Napolitano of Reason, the government started in 1911 to do what economists call ‘rolling over the debt, that is, borrowing more money to pay its lenders, rather than using tax revenue to pay back the debt. Napolitano appears to have a very negative perspective of Wilson, proclaiming

President Woodrow Wilson—who gave us a racially segregated military and federal civilian workforce, brought us into the horrific and useless World War I, arrested Americans for singing German beer hall songs in public, campaigned for the federal income tax by promising it would never exceed 3 percent of income, helped to create the cash-printing Federal Reserve, laid the groundwork for Prohibition, and kept Jim Crow going—borrowed $30 billion to pay for World War I. That money was borrowed from investors and from the Federal Reserve, which in those days literally printed the cash that it lent.

The $30 billion that Wilson borrowed was repaid by the feds with borrowed dollars. And the folks who lent the feds those dollars were in turn repaid with borrowed dollars. That inflationary cycle has been repeated countless times since all this borrowing from Peter to pay Paul became the financing method of choice for the feds.

As a result of this, the federal government still owes the $30 billion that Wilson borrowed, but it owes it— obviously—to different lenders from those who originally financed the Great War. It has paid more than $15 billion in interest payments on that $30 billion.

Who could run a household or a business the way the feds have run the government in the past 100 years?

That’s the beginning of the end, according to Napolitano, but we must not forget the President who served under the next World War, Franklin D. Roosevelt, the first U.S. President to govern for three terms. Daniel Carr puts a lot of focus on FDR’s influence on the debt when he asserts that ‘The Federal Reserve Bank’s actions, and FDR’s resulting bailout, set in motion the ultimate debt-enslavement of the US Government and its citizens,’ along with this delightful graph.

No mention of Woodrow Wilson is mentioned in the article, but it describes in depth how the Federal Reserve Bank and FDR’s gold confiscation contributed to the increase in the federal debt. This, in essence, has to do with the substitution of paper money for metal money. In the 1800s, people were highly sceptical of this idea, but it came to be more accepted at the end of the century and the beginning of the 1900s, as they began to trust the ability to transfer the paper money back to gold at the US Treasury or at any Federal Reserve Bank at any time, as it even stood so on the government printed money. Austrian economist Ludwig von Mises, however, remained skeptical to attempts to leave the gold standard when he wrote in 1949 (Human Action: p. 471),

The significance of the fact that the gold standard makes the increase in the supply of gold depend upon the profitability of producing gold is, of course, that it limits the government’s power to resort to inflation. The gold standard makes the determination of money’s purchasing power independent of the changing ambitions and doctrines of political parties and pressure groups. This is not a defect of the gold standard; it is its main excellence. Every method of manipulating purchasing power is by necessity arbitrary. All methods recommended for the discovery of an allegedly objective and “scientific” yardstick for monetary manipulation are based on the illusion that changes in purchasing power can be “measured.” The gold standard removes the determination of cash-induced changes in purchasing power from the political arena. Its general acceptance requires the acknowledgement of the truth that on cannot make all people richer by printing money. The abhorrence of the gold standard is inspired by the superstition that omnipotent governments can create wealth out of little scraps of paper.

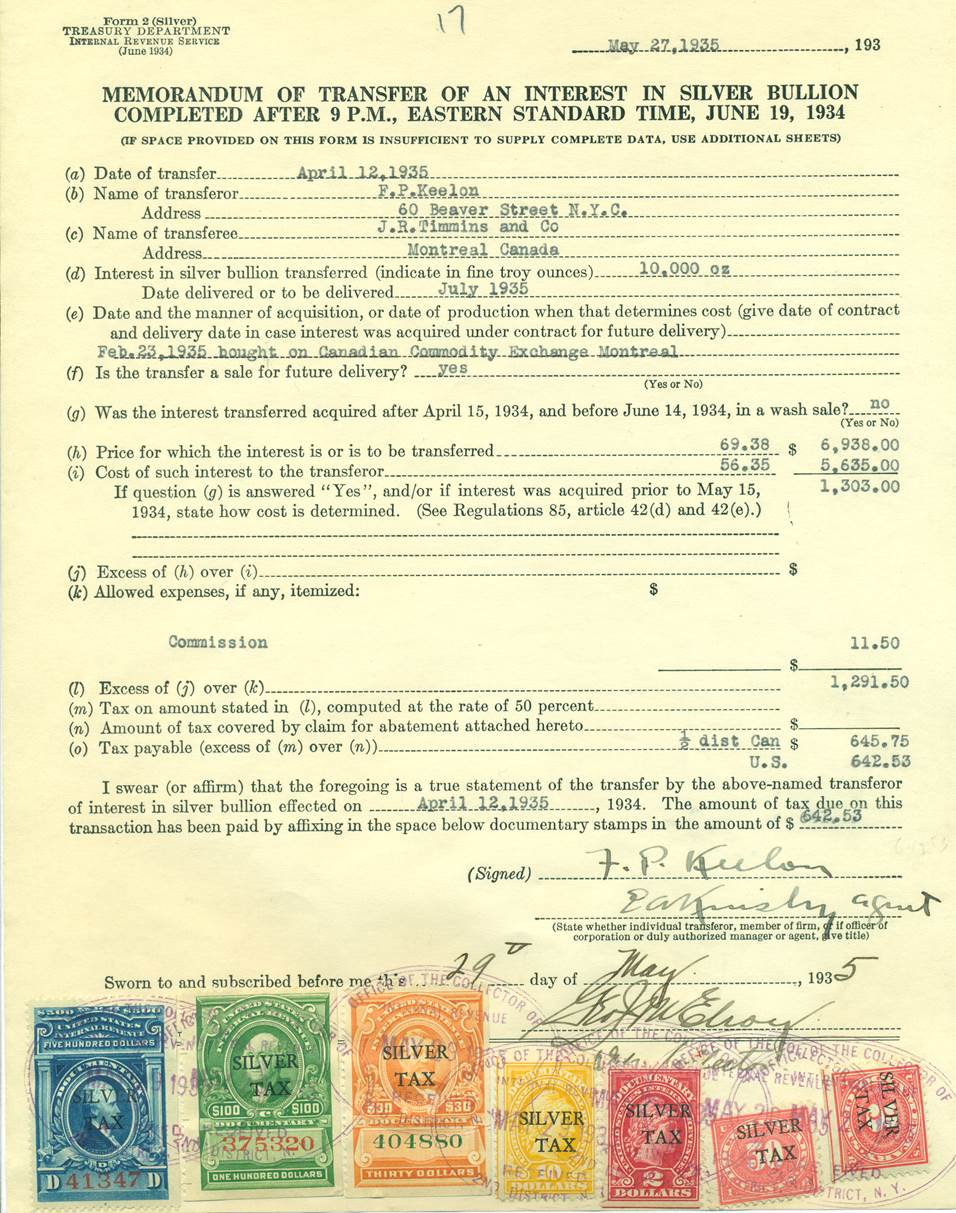

That’s what they tried to do in the beginning of the 1900s, however, and ‘the result,’ asserts Carr, ‘was an economic “boom”, also known as “The Roaring Twenties” (1923-1929). But like all artificially-induced stimulus, it came to a crash in the fall of 1929. The burden of over-extended credit was the culprit.’ Then, when FDR came to power, he outlawed private ownership of gold in an executive order in 1933, forcing citizens to turn in gold for paper money. He also wanted to do this with silver, but as banning silver would be bad for commerce, it was rather placed a 50% tax on the profit of the transfer of silver bullions in 1934 in the Silver Tax Act, which lasted until 1963. This was not the only marks he left on the economy, however, as he holds the record of signing 3,734 executive orders during his reign, and is known for having initiated the New Deal Programs, which have since been both praised and condemned. It had a significant mark on the national debt, however, as it increased from $22.5 billion to $258 billion. FDR justified this in a speech, where he insisted that ‘Our national debt after all is an internal debt owed not only by the Nation but to the Nation. If our children have to pay interest on it they will pay that interest to themselves. A reasonable internal debt will not impoverish our children or put the Nation into bankruptcy.’

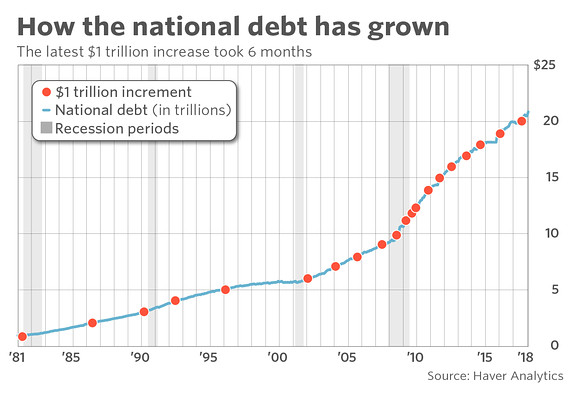

In the aftermath of the Second World War, the federal debt grew gradually, and reached $300 billion by the year John F. Kennedy was assassinated in 1963 and Lyndon B. Johnson took over. It continued up towards $500 billion by Gerald Ford’s term, and under Carter approached the landmark $1 trillion as Reagan entered the arena.

Reagan was a firm advocate of supply-side economics, and thus thought that the most effective plan for economic growth would be to decrease taxes and reduce regulations. As he assumed office, he exclaimed that ‘We don’t have a trillion-dollar debt because we haven’t taxed enough; we have a trillion-dollar debt because we spend too much.’ One would expect, then, that he would know how to deal with it and manage to reduce it, but instead, he tripled it, and left George H. W. Bush with almost $3 billion in federal debt. How could this happen? Reagan left his promise to balance the budget by 1964 on November 6, 1981, claiming that ‘I’ve never said anything but that it was a goal. And the eventual goal, whether it comes then 1984 or whether it has to be delayed or not, is a balanced budget.’ Chris Edwards of the Cato Institute says that ‘Reagan’s failure was that he did not control federal spending growth. By 1989, federal spending was up 69 percent from 1981. The deficit widened, then narrowed again by the end of the decade.’ Cutting taxes in itself doesn’t help the federal debt, and cutting taxes and spending equally only evens things out. As he cut spending on social security programs, however, he also increased the defense budget in light of the cold war. Sheldon L. Richman commented on taxation under Reagan in 1988, ‘If government cuts taxes, but not spending, it still gets the money from somewhere—either by borrowing or inflating. Either method robs the productive sector,’ adding on spending that ‘His budget cuts were actually cuts in projected spending, not absolute cuts in current spending levels. As Reagan put it, “We’re not attempting to cut either spending or taxing levels below that which we presently have.”‘ He also claims that even Carter and Ford did a better job in cutting the power of the government. His economic policy has elsewhere been termed ‘voodoo economics’ for trying to cut taxes while simultanously maintaining or increasing current spending levels. The problem can be illustrated on a graph of the national debt as % of GDP.

From here, a lot of the story speaks for itself. The debt increased to $4 trillion under George H. W. Bush, $5.8 trillion under Clinton, $12 trillion under George W. Bush and $20 trillion under Obama. Don’t trust the voodoo, it’s a trap! Before we end off, however, some notes will be added on the financial crisis of 2008 and its influence on the federal debt.

How, and why, did the financial crisis happen? J. Lewis of Mic, who has read and reviewed dozens of books on the topic, attempted to answer that question in 2012. He explicitly rejects the arguments of it being the cause of deregulation or greedy bankers (as the Occupy Wall Street movement bought), and rather claims that

The most salient explanations for the financial crisis are those that contextualize it within the broader systemic framework of our country’s ongoing debt crisis. As cheap money flowed into the United States from abroad, it was diverted into the housing sector, leading to an increase in home prices, leading to an asset boom and subsequent bust. It was only a matter of time from when housing prices plummeted until market uncertainty as to the value of mortgage-backed securities reigned. This is not to say that flawed federal housing policy and Wall Street recklessness did not contribute to the crisis. They did, but only within the greater context of mistakes in fiscal and monetary policy.

In 2008 Bush signed the Emergency Economic Stabilization Act of 2008, authorizing the Department of Treasury to bail out the banks and purchase distressed assets like mortgage-backed securities in an effort to fix the problem. Economists were skeptical to this solution, however. On September 24 the same year, 100 university economists sent an open letter to Congress informing them that they expressed ‘great concern for the plan proposed by Treasury Secretary Paulson,’ and described three ‘fatal pitfalls’ in the plan:

- It’s unfair, as it subsidizes investors at the expense of the taxpayers;

- Neither its mission nor its oversight are clear; and

- It’s shortsighted, as it appears to solve the current problem, but its effects will remain for a generation.

The letter was endorsed by 231 economists at American universities, and was described as ‘the emerging consensus from academic economists.’

Then emerged Obama, whose increase to $20 trillion leaves us where we are today. So, what policies created the biggest increase in the debt? It was five-fold, according to The Balance.

- Obama’s tax-cuts, which as an extension of Bush’s tax cuts added $857 billion;

- The American Recovery and Reinvestment Act, the fiscal stimulus which ended the great recession, added $787 billion between 2009 and 2012;

- Around $800 billion increase in spending to the military ever year; and

- The Patient Protection and Affordable Care Act didn’t add anything to the debt before health insurance exchanges opened in 2014.

In defense of Obama, and presidents throughout American history in general, they opine,

Is it fair to blame any president for events over which he had no control? During Obama’s terms, there was less federal income than usual. The recession and the Bush tax cuts reduced tax receipts. At the same time, the cost of Social Security, Medicare, and other mandatory programs continued to increase. The War on Terror, although technically over, was still being fought in Afghanistan and Iraq.

We’ve now taken a little look of main key points of the history of the American Federal Debt. The purpose of this article has not been to bring all the details to the table, as that would require a lot more space, but rather to spark some reflection and debate on how the federal debt arrived at the point it has, and what could effectively be done to plateau it or even reverse it. We’ve gotten some hints by this analysis of history, like balancing the budget, and avoiding voodoo economics by cutting spending more than taxes. As said, this article has tried to bring a general picture, but it is not the full story, so, as Horace proposes, ‘dare to know,’ and continue seeking out the truth and solutions of the problems plaguing the present.

_____________________________________________________

Stefan M. Kløvning is the Deputy Operations Manager of Goldfire Media and has written over 70 articles since joining the team in September 2017. He writes primarily on politics and economics, but also has interest in a large array of other fields. Stefan was formerly leaning left politically, but moved more to the right during 2017 and joined the libertarian Progress Party in Norway at the end of the year.